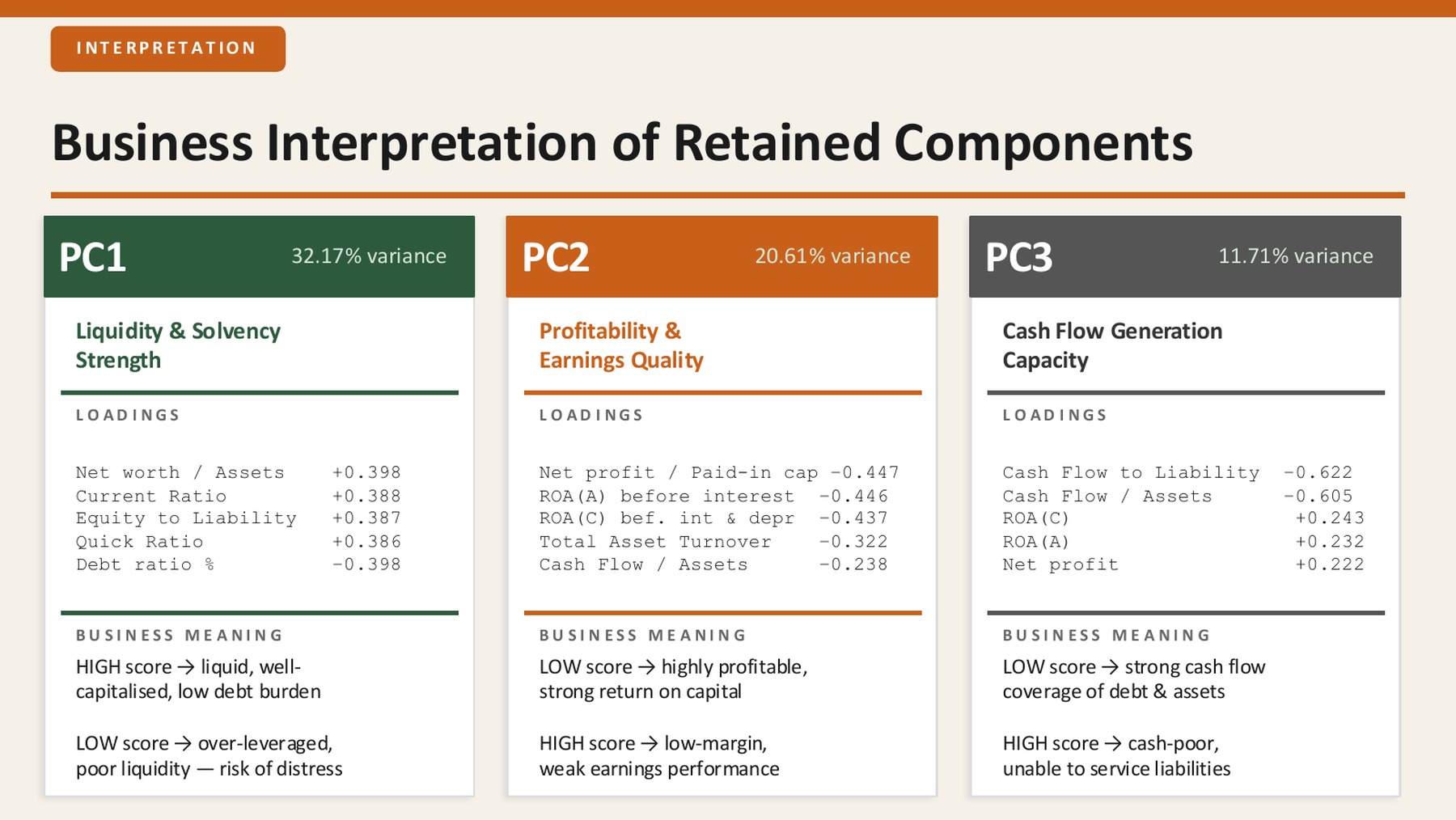

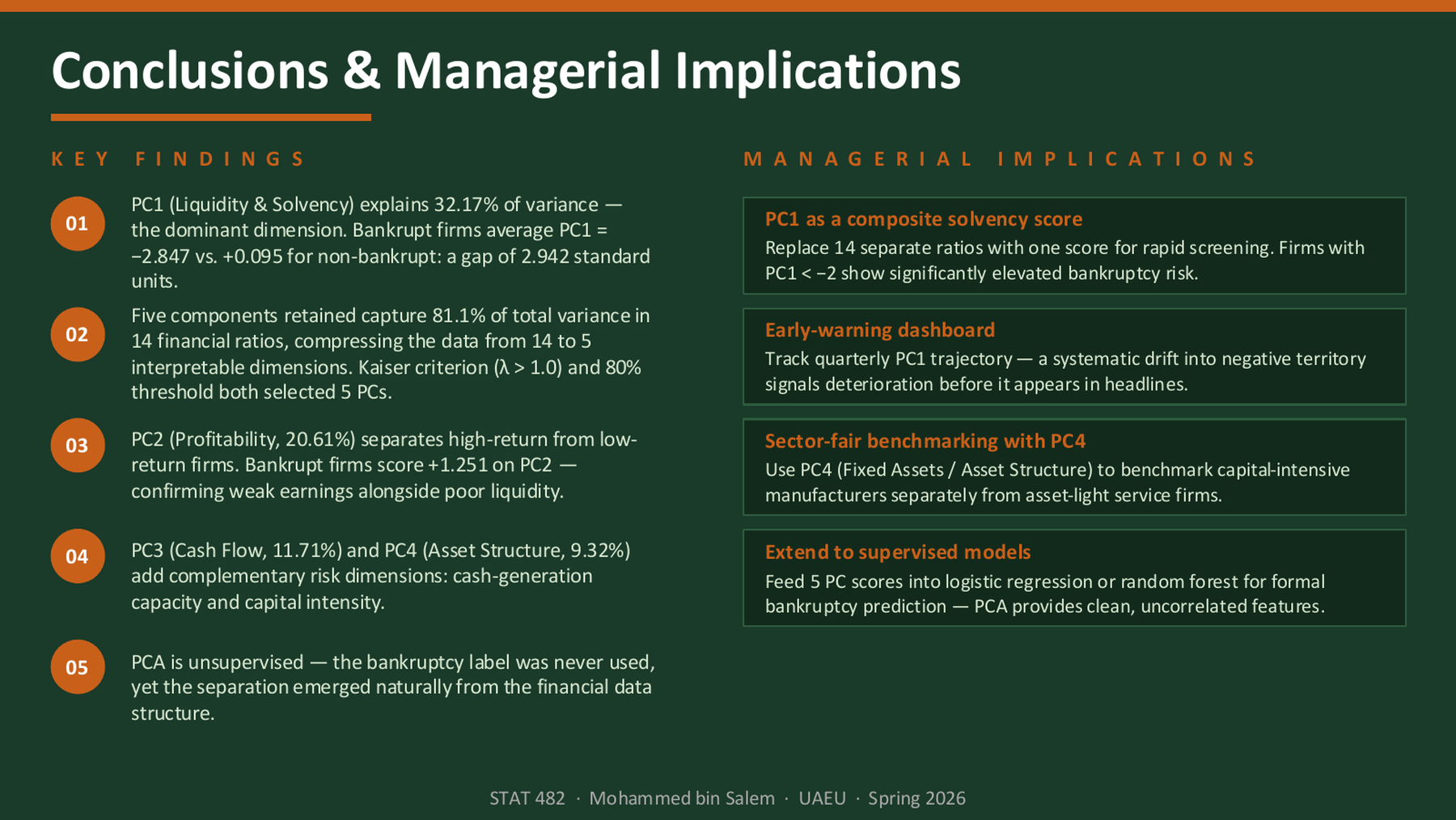

I used PCA to make firm performance interpretable

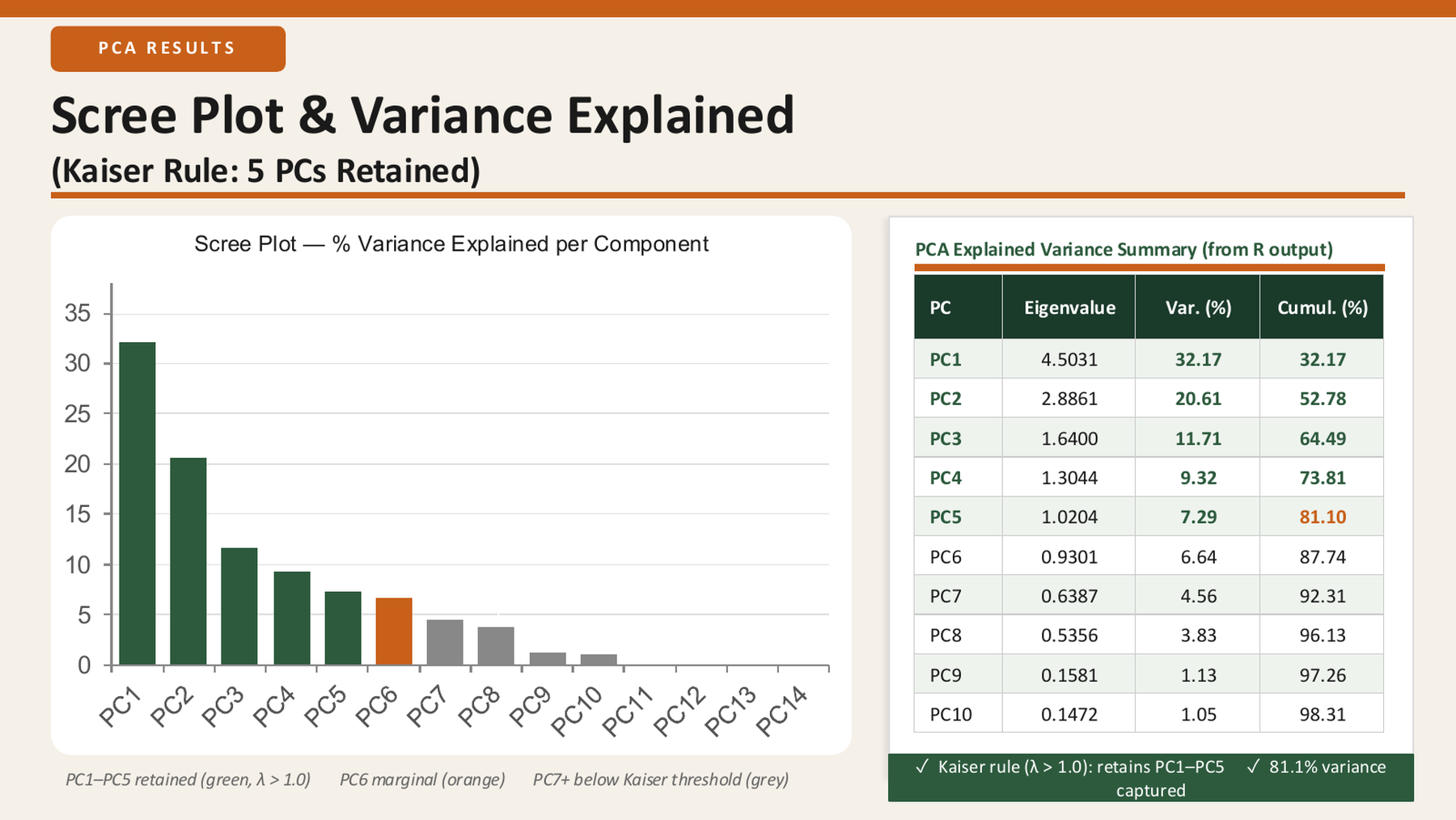

I framed this project around a practical finance question: when a firm has dozens of financial ratios, which underlying dimensions actually explain performance? PCA helped me move from a crowded ratio table to a smaller set of interpretable business signals. The goal was not to predict bankruptcy directly, because the bankruptcy label was excluded from the PCA inputs. The goal was to discover structure first, then test whether that structure made financial sense.