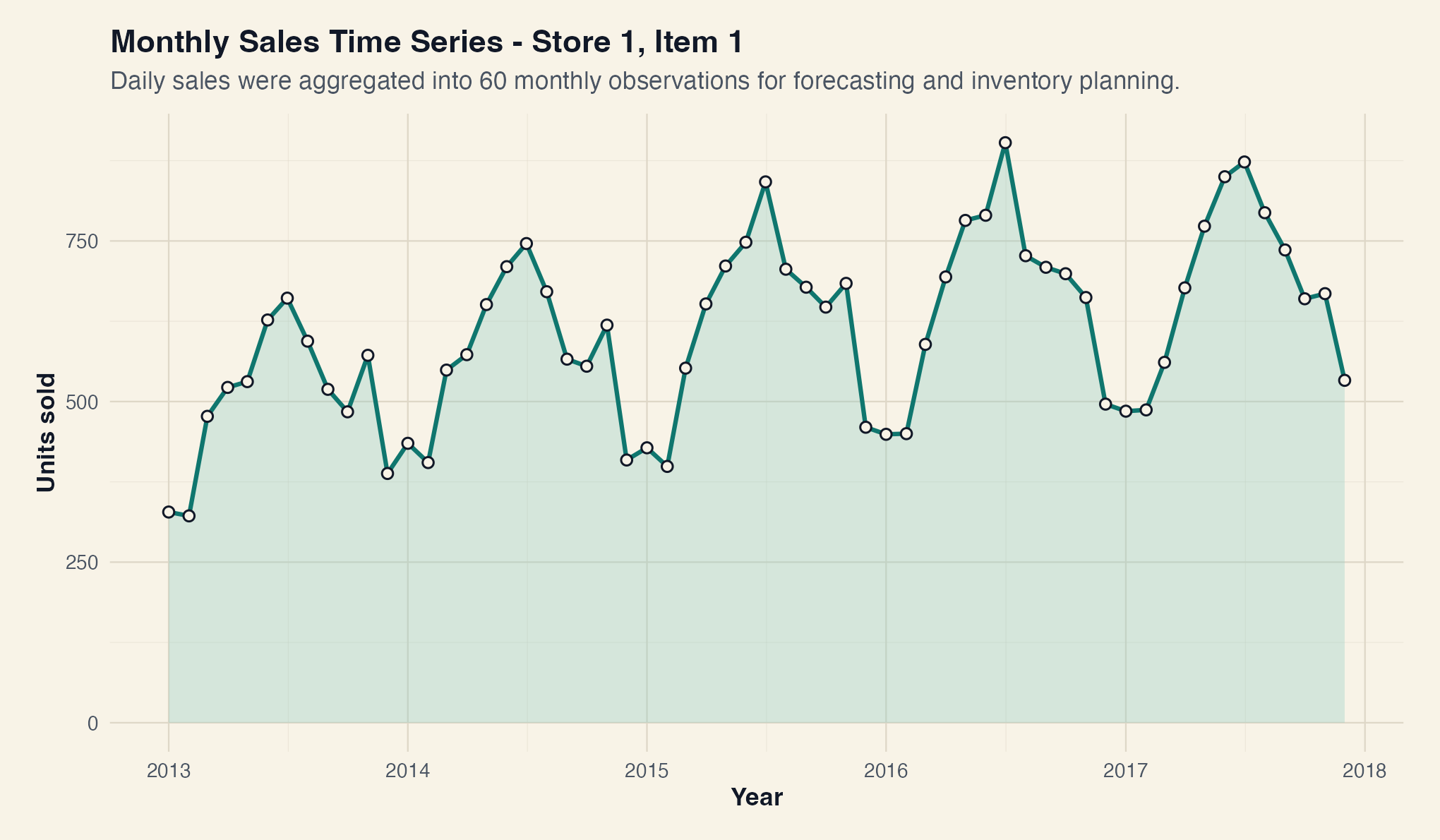

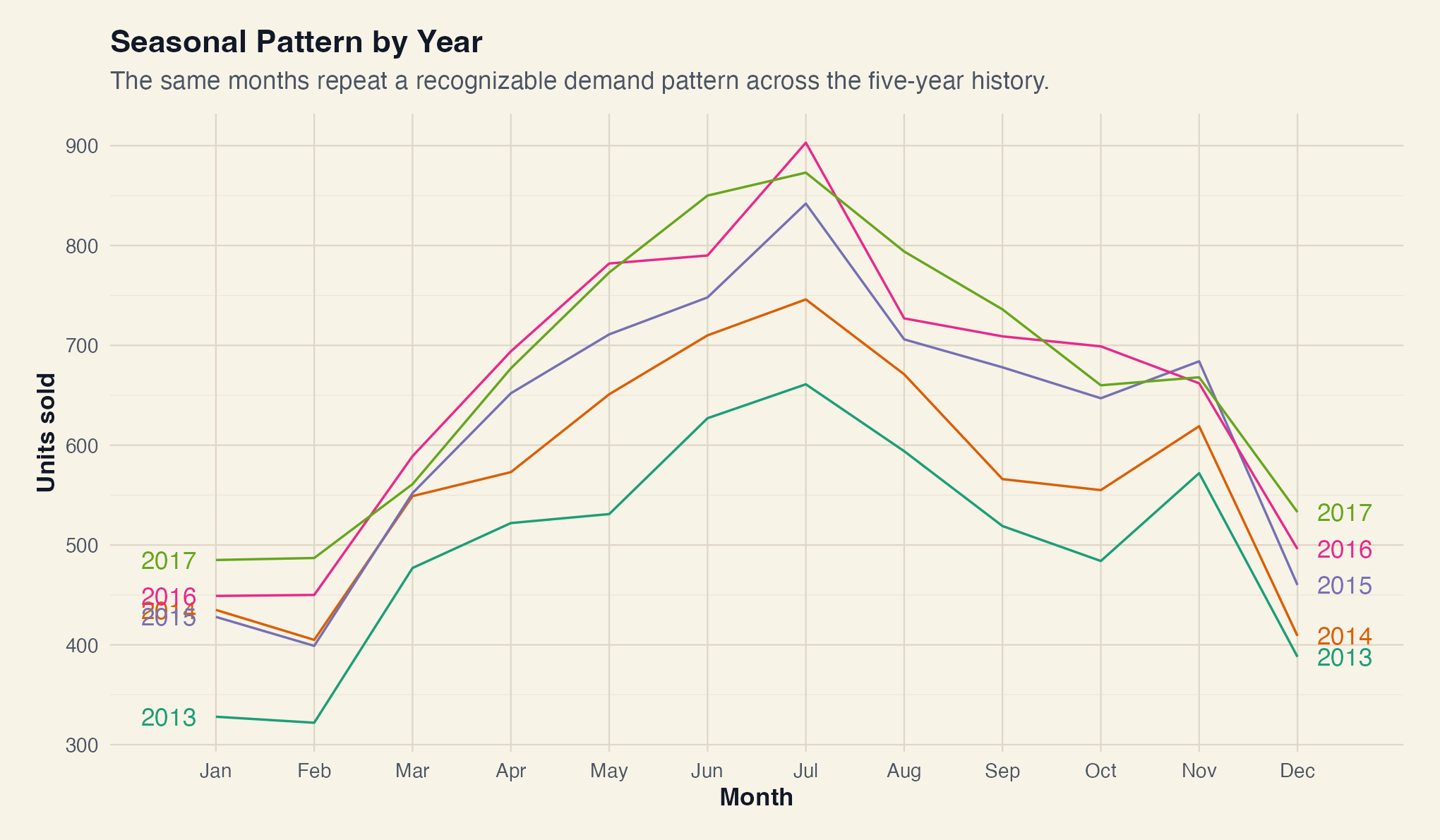

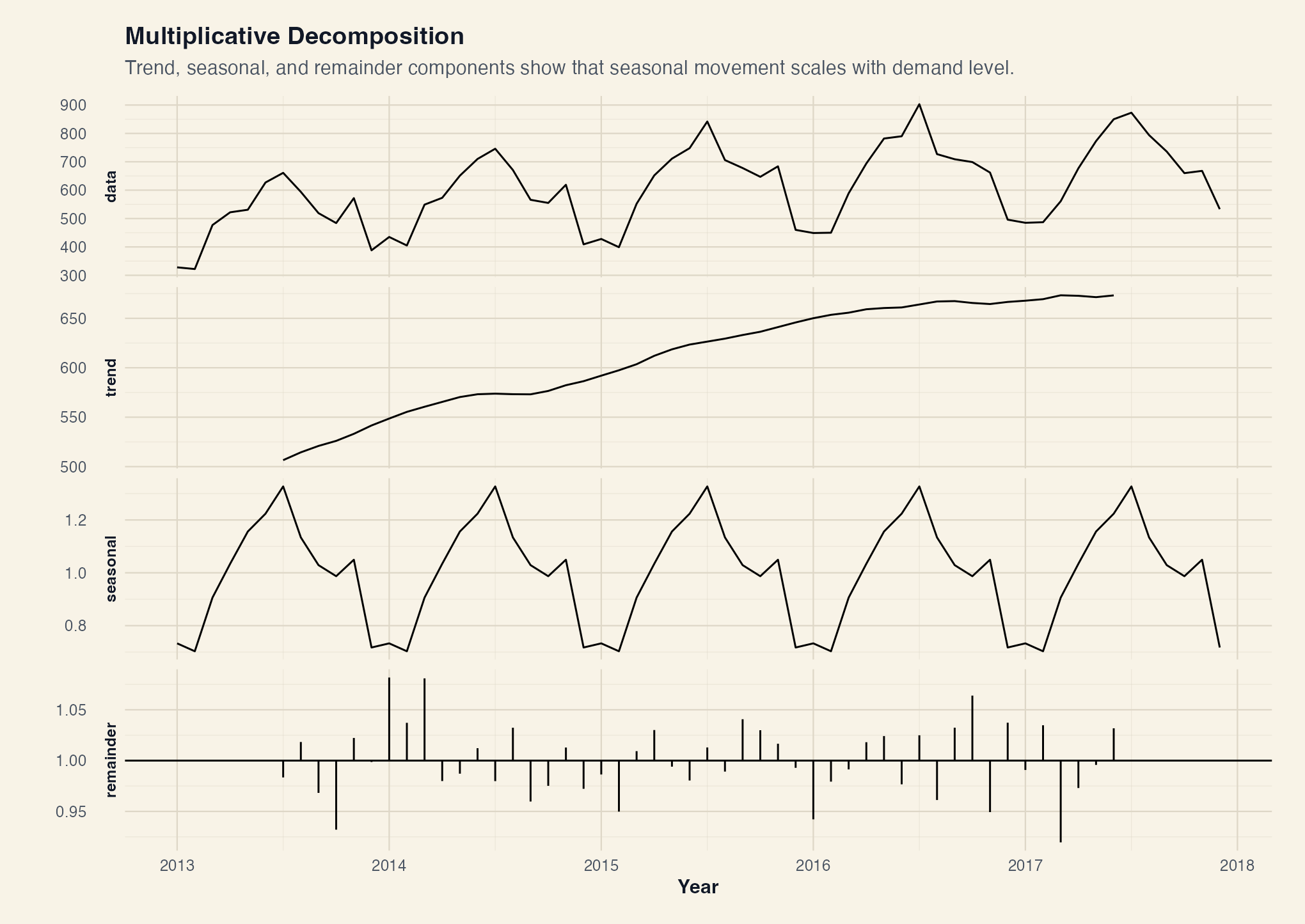

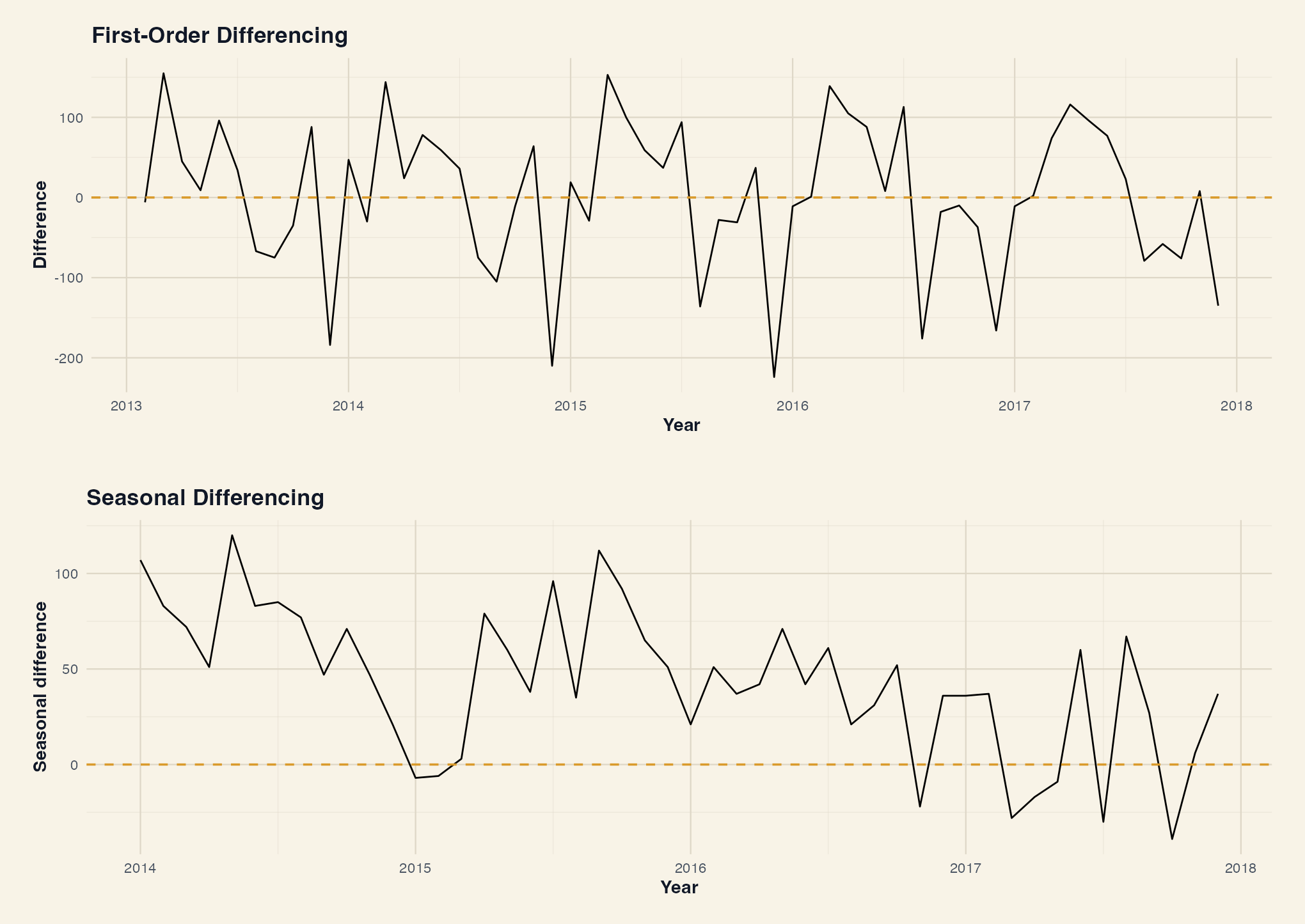

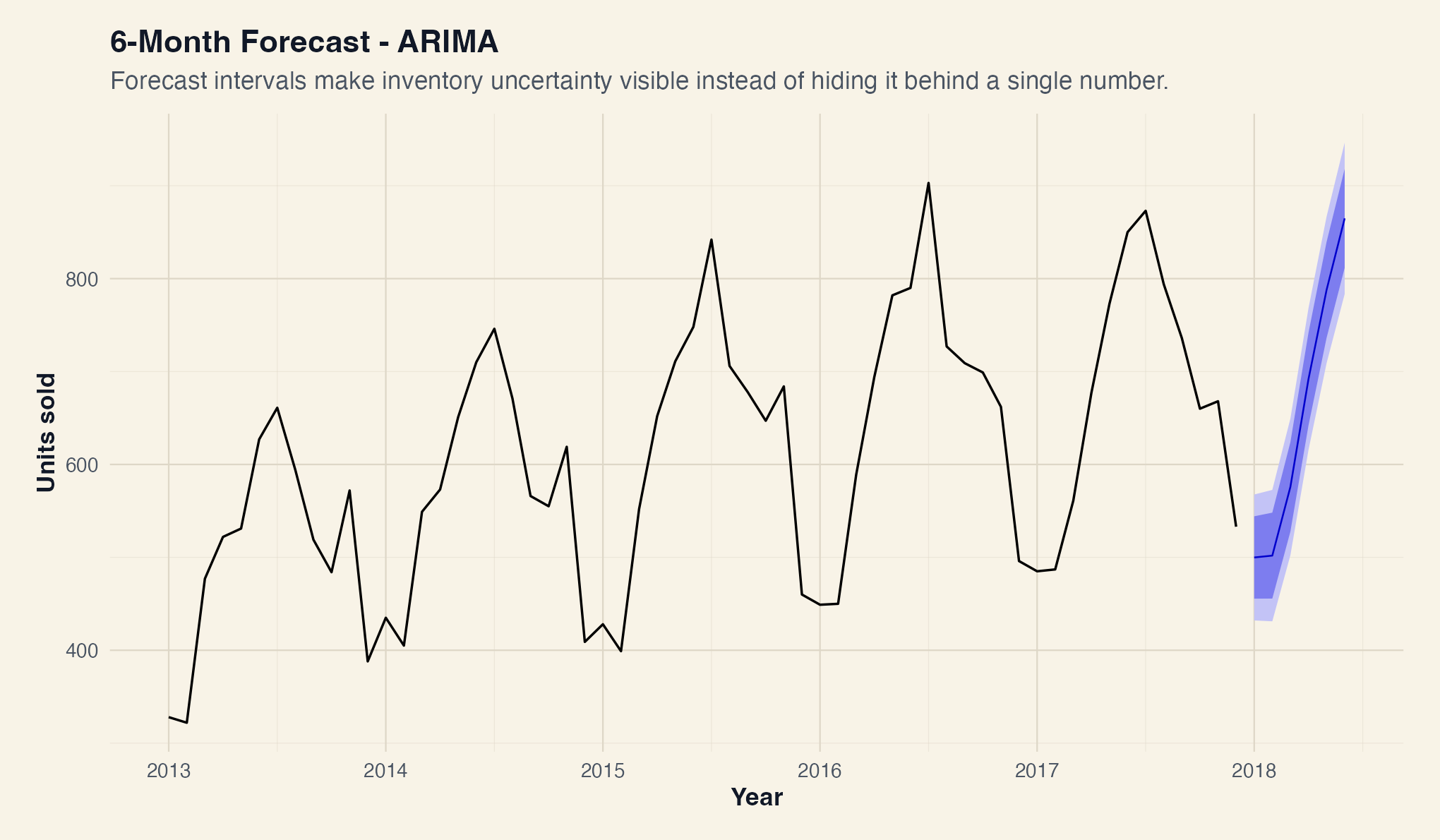

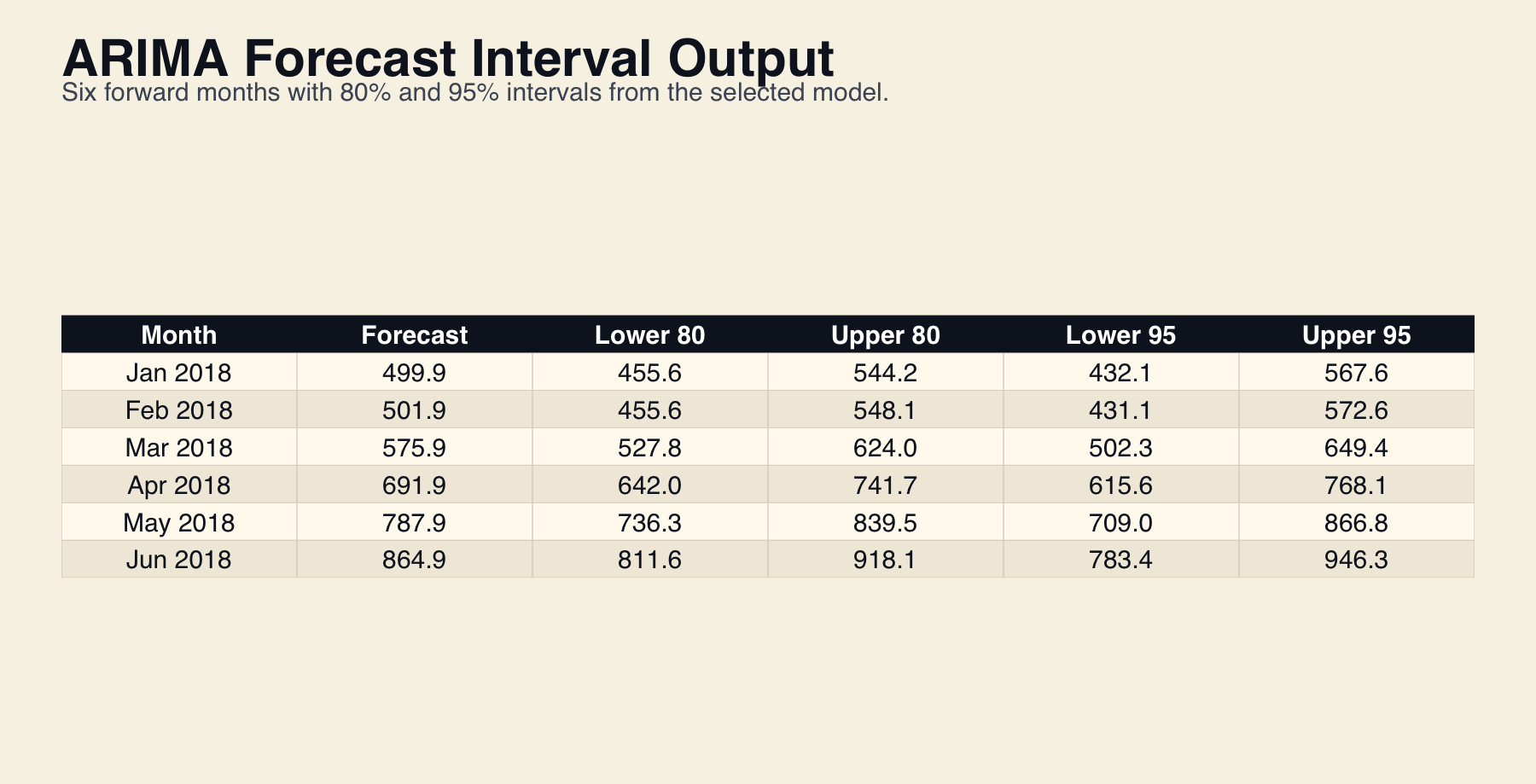

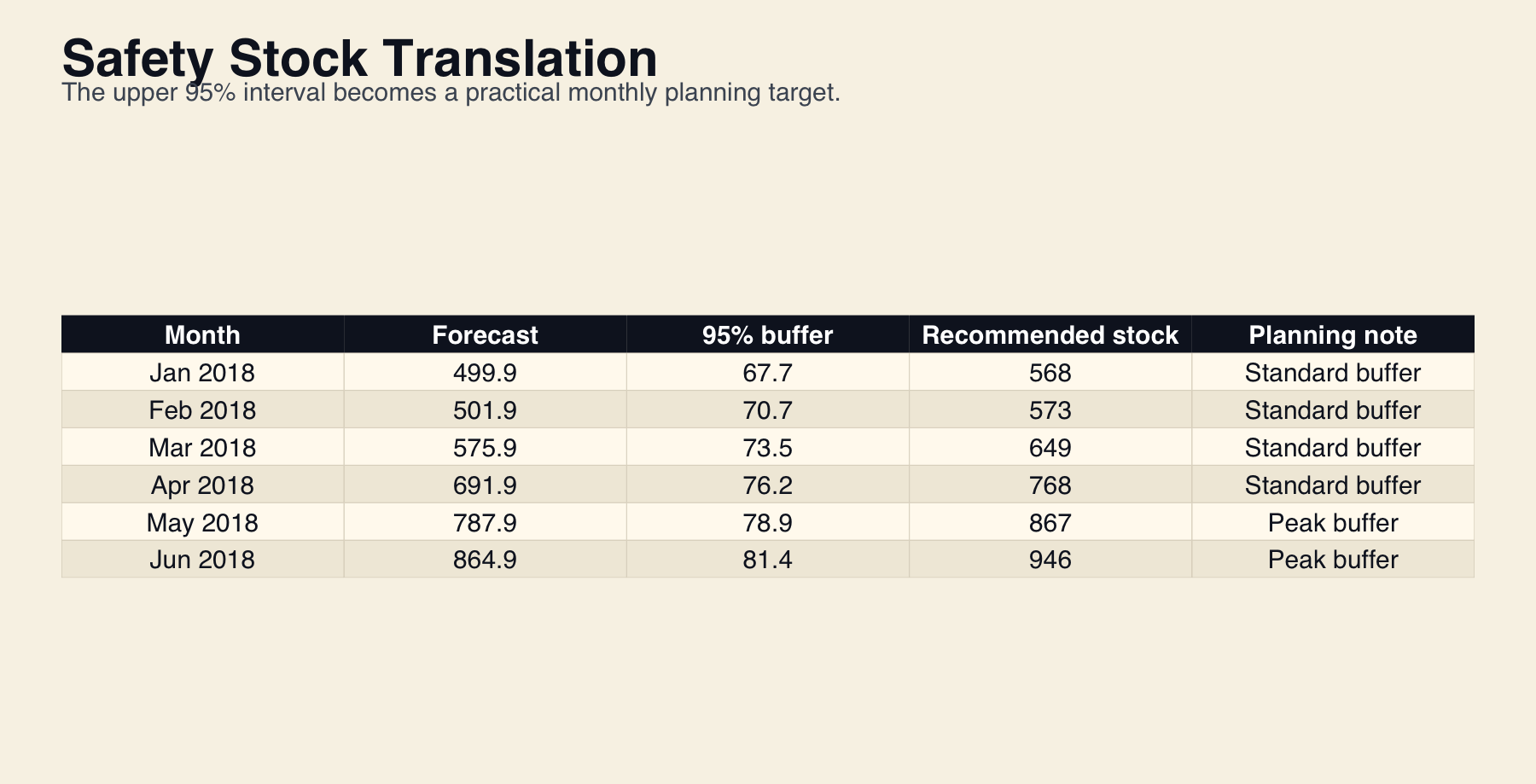

I started with the inventory decision

The case starts with a practical operating question: how much demand should the company prepare for next month and the months after that? I framed forecasting as an inventory decision instead of a purely statistical exercise. That kept the model comparison grounded in stockouts, overstock, reorder planning, and the value of forecast uncertainty.